Published October 15, 2025

When the Fed Cuts: What Federal Rate Cuts Could Mean for Edmond & OKC Real Estate

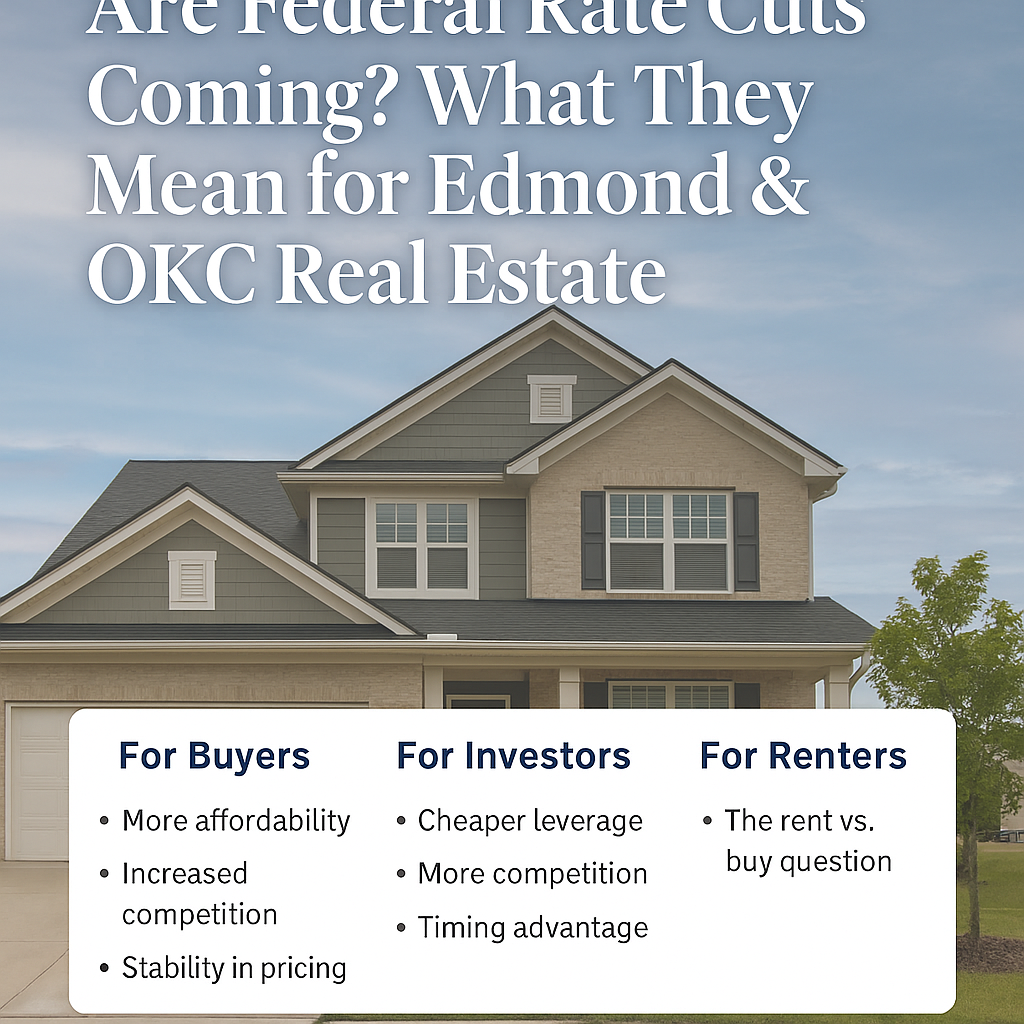

Interest rates set by the Federal Reserve do not just live in the headlines — they ripple through mortgage rates, credit costs, investor behavior, and ultimately, local real estate markets. With expectations growing for one or two rate cuts in late 2025, now is a good time to explore how such cuts might affect homebuyers and real estate investors—especially in the Edmond and Oklahoma City metro areas. Could this be the moment first-time buyers move off the sidelines? Should investors pounce now? Let us dig in.

What is the current rate environment & what cuts are expected?

First, a quick status check:

- As of the Fed’s September 17, 2025 meeting, it lowered its target federal funds rate by 25 basis points (0.25 %) to 4.00 %–4.25 %.

- The Fed’s summary of economic projections (dot plot) implies that many members expect two more cuts this year, perhaps another 0.25 % at each of the remaining meetings.

- Some analysts are more aggressive, projecting deeper cuts (e.g. Goldman Sachs sees multiple cuts through year-end).

- However, uncertainties remain: inflation is not fully tamed, and some Fed officials caution against cutting too aggressively.

- Mortgage rates, which matter more for homebuyers than the federal funds rate directly, don’t always move in lockstep with Fed rate changes. Many external factors (bond yields, credit markets, inflation expectations) also exert influence.

So the baseline assumption: one or two modest cuts in the latter half of 2025, likely 25 basis points apiece, with more in 2026 depending on economic data.

How do one or two rate cuts affect real estate, especially locally?

It’s tempting to think “rate cut → mortgage rates fall → everyone buys” — but the dynamics are more nuanced. Below, I explore the channels by which rate cuts can influence housing—and how those might play out in Edmond / OKC metro.

Mechanisms & timing

- Mortgage rate pressures

- Lower short-term rates tend to ease financial conditions, pushing down yields on longer-term bonds (such as the 10-year Treasury). Mortgage rates often follow Treasury yields (with some spread).

- However, mortgage rates are also affected by credit risk, demand for mortgage-backed securities, inflation expectations, and lender margins. So even if the Fed cuts, mortgage rates might not fall as much as desired, or they may lag.

- A 0.25 % cut by the Fed does not guarantee a 0.25 % drop in mortgage rates — sometimes the pass-through is dampened.

- Consumer affordability & demand

- Lower interest rates reduce monthly payments for new mortgages, thereby increasing affordability for a given price. This can expand the pool of potential buyers.

- Buyers with floating-rate debt (or adjustable-rate mortgages nearing reset) may feel relief or less downward pressure.

- The psychological encouragement of a “rate easing” cycle may draw hesitant buyers off the sidelines.

- Investor and developer behavior

- Real estate investors often leverage debt; cheaper financing raises their yields and may stimulate more acquisitions or development activity.

- On the supply side, developers may accelerate projects if financing costs drop, increasing inventory in certain segments.

- However, for existing homeowners with locked-in low rates, the incentive to sell may be weaker unless they must upsize or relocate.

- Price pressures and competition

- If demand rises (due to better affordability) while supply remains constrained, prices can rise, especially in desirable submarkets.

- In areas where supply is more elastic or where new construction is possible, increased inventory might temper price appreciation.

Specific to Edmond / OKC metro

In the context of Edmond and the broader OKC area, some local factors will mediate how strongly rate cuts translate into market movement:

- Current housing metrics: In August 2025, Oklahoma’s median home sale price was ~$254,100 (up ~1.2 % year-over-year) and homes were averaging ~42 days on the market.

- Inventory dynamics: In OKC metro, some reports suggest elevated inventory growth compared to prior years, meaning buyers might have more options than in peak times.

- Affordability constraints: While home values are not skyrocketing locally, mortgage rates in recent years have been high enough to strain affordability for many buyers. A modest cut could meaningfully improve what buyers can qualify for.

- Local economic fundamentals: Job growth, wage growth, population trends, and local industries (energy, aerospace, etc.) will influence whether more people move to the area and demand housing.

- Geographic/submarket variation: Edmond tends to have desirable school districts, stability, and demand; smaller or less desirable peripheral markets may respond differently.

Taken together: a modest rate cut or two could stimulate additional demand in Edmond / OKC, especially in strong neighborhoods, but the upside may be tempered in less desirable pockets or overpriced segments.

Should investors act now?

If you’re an investor (residential rental, flips, multi-family, etc.), here are the pros, cautions, and timing considerations:

Pros of acting now / pre-emptively

- Lock in current inventory before competition intensifies: If rate cuts ignite more buyer demand, deals may be harder to find or bargain prices may shrink.

- Better yields: Lower financing costs can boost net yields and make more marginal projects viable.

- First-mover advantage: In underperforming or transitional markets, you may capture growth early.

- Hedge against future inflation: Real estate can act as an inflation hedge; if the Fed cuts, inflation risk tends to increase, favoring real assets.

Risks and cautions

- Rates might not fall as much or as fast as expected: If mortgage rates remain sticky, your financing costs may not drop meaningfully.

- Overpaying risk: Buying too aggressively now when the market is still constrained might lead to downside if sentiment sours.

- Operational and vacancy risk: If local rents or demand don’t keep pace, your cash flows may suffer.

- Economic reversal: If inflation surges or an external shock hits, rate cuts may be paused or reversed, hurting real estate valuations.

Strategy suggestions

- Focus on lower-leverage deals to reduce risk.

- Target neighborhoods in Edmond / OKC metro with strong fundamentals (schools, access, growth corridors).

- Lock in financing now if you believe rates will rise again.

- Be selective — don’t chase every deal as rates drop; maintain discipline on yields and exit strategies.

- Consider phased deployment — perhaps acquire one property now and hold cash reserves to pounce when cuts arrive.

In short: yes, this is a favorable window, but don’t rush blindly. The best investors will be those who combine boldness with prudence.

Is this a great time for first-time homebuyers to buy rather than rent?

This is one of the more compelling questions, because the balance between “renting vs buying” often comes down to interest rates, time horizon, and local conditions.

Why this could be a strong moment

- Affordability boost from lower rates

- If mortgage interest rates drop, that means lower monthly payments for the same principal amount. For many first-time buyers, that difference can make or break eligibility or comfort level.

- In markets like OKC / Edmond, where home price appreciation has been moderate (vs coastal metros), a lower rate may tip the balance.

- Locking in price vs rent inflation

- If you expect rents to rise over time (which is common), buying allows you to lock in your “housing cost” (aside from property taxes, insurance, maintenance).

- Over a longer time horizon, equity buildup and appreciation can make buying more favorable.

- Building equity & forced savings

- Paying a mortgage forces you to build equity, whereas rent payments go entirely to the landlord.

- Down payment / closing cost challenges

- This often remains the main barrier. Even if interest rates are favorable, coming up with that initial capital is the hurdle for many.

- First-time buyer assistance programs, local grants, and lower down-payment mortgage options can help.

Where the caution lies

- Short-term mobility: If you know you’ll move within a few years, the transaction costs (closing, selling, commissions) may negate the benefits.

- Maintenance, property taxes, insurance: Owning carries additional costs (roof, systems, upkeep) that renters don’t face directly.

- Interest rate volatility: If you buy now and rates fall further, early buyers may feel remorse seeing their mortgage terms “too high.”

- Local market risk: If prices stagnate or decline in some submarkets, a buyer can see little upside in the near term.

So, should first-time buyers buy now?

Given modest expected rate cuts, improving affordability, and relatively stable pricing in OK markets, this could indeed be a favorable window for first-time buyers. In particular:

- If you plan to stay in the home for 5–10 years or more, the long-term benefits often outweigh short-term costs.

- If you can qualify now with a manageable payment and still keep reserves for repairs, that’s a strong position.

- If you can time some of your home search around rate cuts (e.g. locking just after a cut) that may help, but don’t let waiting indefinitely lead you to miss out.

One nuance: some buyers may try to time the “bottom” post cuts, but housing markets often anticipate rate cuts (i.e. part of the benefit is priced in ahead of time). So waiting might cost you in terms of home price appreciation.

A few illustrative scenarios

Here’s a simplified illustrative comparison to show sensitivity (very roughly):

|

Scenario |

Mortgage rate |

Loan amount |

Monthly principal + interest |

Notes |

|

Before cut |

6.00 % |

$300,000 |

~$1,799 |

Baseline |

|

After 0.25 % cut (pass-through) |

5.75 % |

$300,000 |

~$1,745 |

Monthly saving ~$54 |

|

After 0.50 % cut |

5.50 % |

$300,000 |

~$1,703 |

Monthly saving ~$96 |

In this example, a single 0.25 % drop gives modest savings; two cuts help more. Over 30 years, even modest monthly differences compound in total interest paid.

Now, if you combine rate cuts plus modest home price appreciation over time, deferred demand, better rental yield or tax benefits, the cumulative effect can tilt the equation further in favor of buying (especially over a 10+ year horizon).

Final thoughts

- Don’t wait too long — there’s risk in sitting out entirely. If you find a home you like and you can afford it with room for buffer, buying now might be better than chasing “lower” rates later and losing deals in the meantime.

- Focus on quality and fundamentals — good neighborhoods, stable demand, schools, transport access—these still matter more than timing the last 0.25–0.50 % of rate movement.

- Lock promptly when favorable — once you get a favorable mortgage offer, locking may make sense rather than speculating on further drops.

- Use local resources — in Edmond / OKC, explore first-time buyer programs, down-payment assistance, or city incentives.

- Be prudent and stress-test your budget — ensure you can handle variations in interest rates, repair costs, or temporary vacancies (if investing).

- Balance risk with optionality — If uncertain, consider partial commitments (e.g. buying a duplex or a smaller home) or keep some liquidity in reserve.

In sum: modest Fed rate cuts (one or two) are unlikely to trigger a housing boom overnight, but they can meaningfully improve affordability and shift sentiment. For Edmond / OKC metro, those effects may be more pronounced in desirable neighborhoods with solid demand fundamentals. For first-time buyers, this window looks quite favorable, especially if you’re in it for the long run. For investors, the upside is real — but success will come down to disciplined underwriting, local market insight, and timing.

Looking forward to the months to come!

Fidelity Real Estate Brokers